The International Tax Law Team at RJS LAW receives numerous inquiries regarding a crucial yet often misunderstood element of United States tax law — IRS Form 8833, or the Treaty-Based Return Position Disclosure. For taxpayers engaged in global transactions, Form 8833 is significant as cross border transactions are often regulated by international tax treaties.

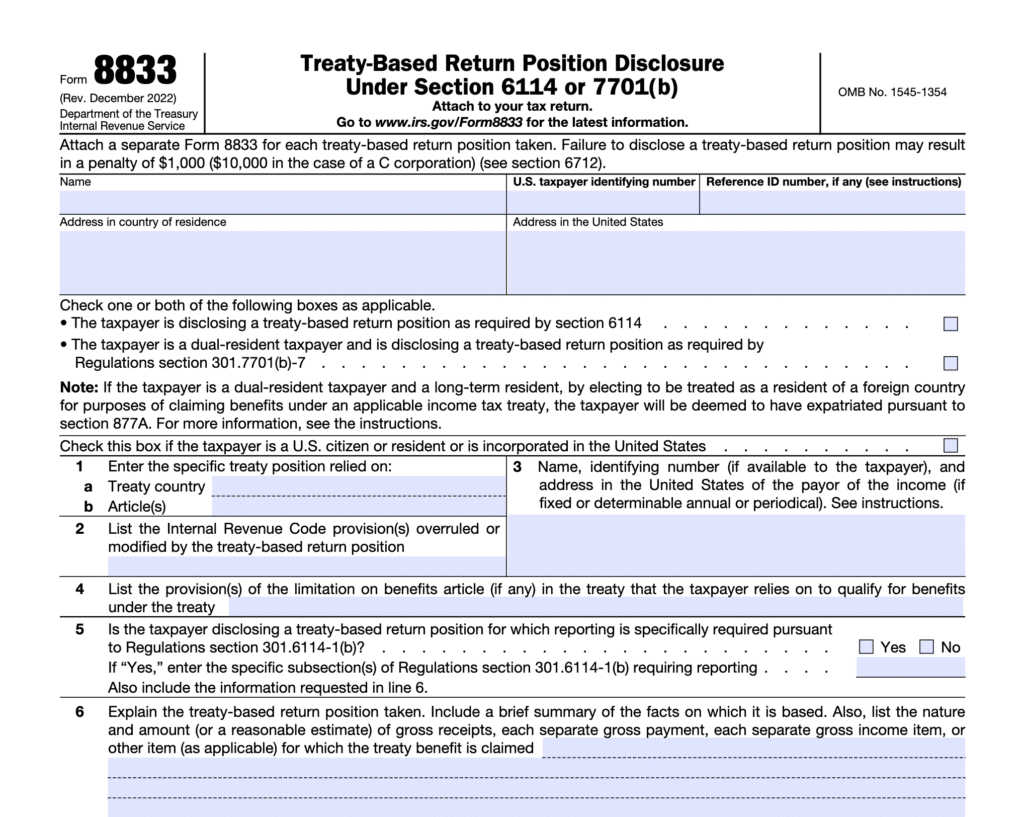

What is Form 8833?

is a tax disclosure document submitted by U.S. taxpayers who take the position that a treaty of the United States supersedes or modifies certain provisions of the Internal Revenue law. The intricacies of international treaties may provide taxpayers with an avenue to navigate around certain tax obligations, thus reducing tax liability. To utilize the potential advantages, taxpayers need to comply with specific disclosure regulations – including the filing of Form 8833.

At its core, Form 8833 comes into play when a U.S. taxpayer, either an individual or a corporation, receives benefits from a foreign country which are non-taxable in the foreign jurisdiction. Under existing U.S. tax law, all citizens and resident aliens are taxed on their worldwide income. This implies that despite the income being earned tax-free in the foreign country, the Internal Revenue Service (IRS) would consider the income as taxable in the U.S. However, in circumstances where a mutual treaty exists, the taxpayer may elect to adopt a treaty position to exclude the income from their U.S. tax return. In such instances, Form 8833 becomes a requisite.

Complexities

Completing Form 8833 requires knowledge of the given treaty invoked, the specific article of the treaty in play, and the segment of the Internal Revenue Code the treaty position overrules, modifies, or exempts. A detailed explanation of how the treaty position provides tax relief to the taxpayer is also crucial. Navigating the various treaty and tax components is not always straightforward and often requires the expertise of an international tax professional to ensure proper compliance.

It is essential to clarify that not all treaty positions mandate the filing of Form 8833. There exist numerous exceptions, exclusions, and limitations taxpayers may rely upon to avoid the completion and filing of Form 8833. For example, under Regulation Section 301.6114-1(c), reporting on Form 8833 is waived for certain treaty-based return positions, such as cases where a treaty reduces or modifies the taxation of income derived by an individual from pensions, annuities, or social security.

Dual-Residents and Form 8833

An interesting scenario often arises for dual-resident taxpayers. If an individual is a resident, for tax purposes, of both the U.S. and another country, they may claim treaty benefits as a resident of the foreign country. In this scenario, the taxpayer would be required to file a Form 8833 along with Form 1040NR or Form 1040NR-EZ within the prescribed reporting deadlines. However, opting to be treated as a resident of a foreign country under an income tax treaty may result in the termination of their U.S. residency status for federal income tax purposes. Consequently, these taxpayers may become subject to tax under Section 877A and would be required to file Form 8854, known as the Initial and Annual Expatriation Statement.

Understanding these complexities is crucial to navigate the landscape of international tax law effectively. Each taxpayer’s set of circumstances must be individually considered to determine the applicability, risks, and potential rewards involved.

Engaging a tax professional well-versed in international tax laws and treaties like the team at RJS LAW can help mitigate risks, ensure compliance, and take advantage of potential tax benefits. Non-compliance may result in severe penalties, including the disallowance of a treaty-based return position by the IRS, offshore tax penalties, and potential loss of U.S. residency for federal income tax purposes. Therefore, when it comes to IRS Form 8833 and international tax treaties, the advice is to understand, comply, and whenever in doubt, consult with a professional.

Written by Andrea Cisneros Valdez, Esq., LL.M.

Leave a Reply