THE GOOD THE BAD AND THE UGLY

California Proposition 19

Proposition 19, formally titled The Home Protection for Seniors, Severely Disabled, Families, and Victims of Wildfire or National Disasters Act (Prop 19) was narrowly passed by California voters on November 3, 2020, with 51.1% of the total vote. Despite Prop 19’s heartwarming title, its primary purpose is to increase home sales throughout California, which will result in increased property tax revenues for counties and more commissions for real estate brokers. Just follow the money. Of the $57,463,195 spent in support of Prop 19, approximately 98% came from the real estate industry with $51.4 million coming from the California Association of Realtors and $4.9 million coming from the National Association of Realtors. $0 was spent in opposition of Prop 19.

Proposition 19 adds Sections 2.1, 2.2, and 2.3 to Article XIII A of the Constitution of the State of California. There are two main components of Prop 19: (1) taxation of inherited property transfers, which takes effect on February 16, 2021, and (2) expanded special rules for eligible homeowners, which takes effect on April 1, 2021.

Taxation of Inherited Property Transfers

Portions of Prop 19 modify Propositions 13 and 58. Proposition 13, passed in 1978, limits property tax increases to 2% per year (1% of the full cash value of the property, and 1% to be collected by the counties and apportioned according to law to the districts within the counties, e.g., certain bond measures ). Proposition 58, passed in 1986, excludes from reassessment transfers of real property between parents and children. Specifically, Proposition 58 allows property owners to transfer their principal residence to their children without the residence being reappraised for property tax purposes and up to $1 million of assessed value of other property (any real property class, including commercial property). In 1996, Proposition 193 expanded Proposition 58 by excluding from reassessment transfers of real property from grandparents to grandchildren, provided that providing that all the parents of the grandchildren who qualify as children of the grandparents are deceased as of the date of the transfer.

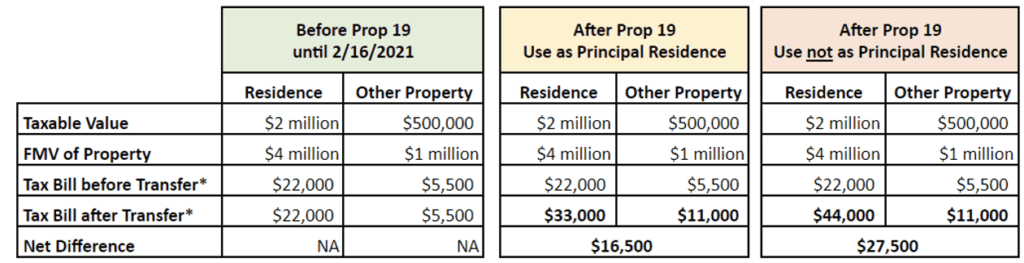

Under Proposition 19, only the transferors principal residence, not other real property, can be transferred to children or qualifying grandchildren at the owners assessed value, provided that the children or qualifying grandchildren use the home as their principal residence and the fair market value of the residence does not exceed the assessed value by more than $1 million. If the assessed value of the family home exceeds the sum of the taxable value plus $1 million, Sections 2.1(c)(1)(A) and (B) require adjustment of the taxable value. For example, parents home has an assessed value of $500,000. Parent dies on February 17, 2021, and the home is inherited by parents only child. The home was the primary residence of both parent and child. On parents date of death, the property has a fair market value of $1,750,000.

1. Calculate the sum of factored base year value plus $1,000,000.

$500,000 + $1,000,000 = $1,500,000

2. Determine whether the assessed value exceeds the sum of the factored based year value plus $1,000,000.

$1,750,000 is greater than $1,500,000

3. Calculate the difference.

$1,750,000 – $1,500,000 = $250,000

4. Add difference to factored base year value,

$500,000 + $250,000 = $750,000

5. New combined based year value = $750,000

The term principal residence means a dwelling for which a homeowners exemption or a disabled veterans residence exemption has been granted in the name of the eligible transferor[1]. This provision of Prop 19 addresses what has been dubbed the Lebowski loophole after The Big Lebowski actor Jeff Bridges and his siblings advertised their inherited Malibu home for rent at nearly $16,000 per month despite paying just a fraction of that amount in annual property tax. Accordingly, the drafters of Prop 19 used class warfare as ammunition for its passage by eliminating unfair tax loopholes used by East Coast investors, celebrities, wealthy non-California residents, and trust fund heirs to avoid paying a fair share of property taxes on vacation homes, income properties, and beachfront rentals they own in California.[2]†The legislators failed to define “fair share.â€

Although the intent of closing “Lebowski loophole, as advertised, was to attack celebrities and trust fund heirs, approximately 99% of California homeowners who inherit a family home are not celebrities or trust fund heirs, so closing the Lebowski loophole will affect them as well. While most wealthy people may be able to pay higher property taxes, many others may not be able to afford the new additional property tax payment. And those unable to pay the new high property tax may be forced to sell the property. Did I mention the real estate industry spent over $56 million in support of Prop 19?

Below is an example of how Prop 19, as it is currently written, would affect children or qualifying grandchildren.

Expanded Rules for Eligible Homeowners

Prop 19 also expands benefits for certain homeowners. Under current law, homeowners over the age of 55 and certain disabled individuals can transfer the taxable value from their current home to a new residence in the same county if the value of the new home is of equal or lesser value than their old home. Effective April 1, 2021, Prop 19 allows those homeowners to transfer the taxable value three times, not just once, and the new home can be anywhere in California so long as it is purchased or newly constructed within two years of the sale of the old home. Victims of wildfires or natural disasters are also eligible under the expanded rules of Prop 19. Prop 19 also eliminated the equal or lesser value requirement. Now, if the assessed value of the new home is equal to or less than the old home assessed value, the base year value transfers to the new home, and if the assessed value of the new home is greater than that of the old home, the new base year value is increased by the difference in fair market value. It is important to note, however, that Prop 19 is unclear whether the sale of the old home and/or the purchase or new construction of the new home must occur on or after April 1, 2021, in order to qualify for the base year value transfer.

Conclusion

Proposition 19 leaves many unanswered questions such as whether existing qualified personal residence trusts will be grandfathered or become invalid. Also, what happens if the child occupies the home as their principal residence, but moves out three, six, or twelve months later? Questions like these, and many others, will be addressed through clarifying statutes, regulations, and further guidance.

There are strategies that can be used to leverage the amount of real estate that can be transferred to children without property tax reassessment, but time is running out. If you have any questions or would like further information regarding Prop 19, contact us today.

[1] California Revenue and Tax Code §63.1(b)

[2] Article XIII A, Section 2.1(a)(2) of the Constitution of the State of California.

[3] 1.1% is used for calculating tax bill on taxable value.

CONTACT

Brian M. Malloy

PRACTICE

Trusts and Estates

Corporate and Business

Real Estate

OFFICE

San Diego

Leave a Reply