International Taxation

In the intricate world of international taxation, one constant remains: the need for accurate reporting and compliance. This is especially true with regard to the W-8 forms, specifically W-8BEN and W-8BEN-E, which are the basis for taxpayers aiming to claim treaty benefits. The recent rise in IRS examination activity makes it crucial to get it right. This blog post aims to demystify these forms and the process surrounding them.

Understanding Tax Treaties

In the realm of international taxation, the term “treaty benefit” is often used and it can sound quite complicated, but it is a straightforward concept.

What is a Treaty Benefit?

A treaty benefit refers to certain tax advantages available to residents or businesses of two countries that have a tax treaty in place. A tax treaty is an agreement between two countries to avoid double taxation—being taxed in both countries on the same income—and to prevent tax evasion.

The Elusive “Valid Treaty Claim”

Claiming treaty benefits is a critical element for both individual and corporate taxpayers but few get it right. A valid treaty claim can significantly reduce withholding tax obligations.

The Anatomy of a Valid Treaty Claim

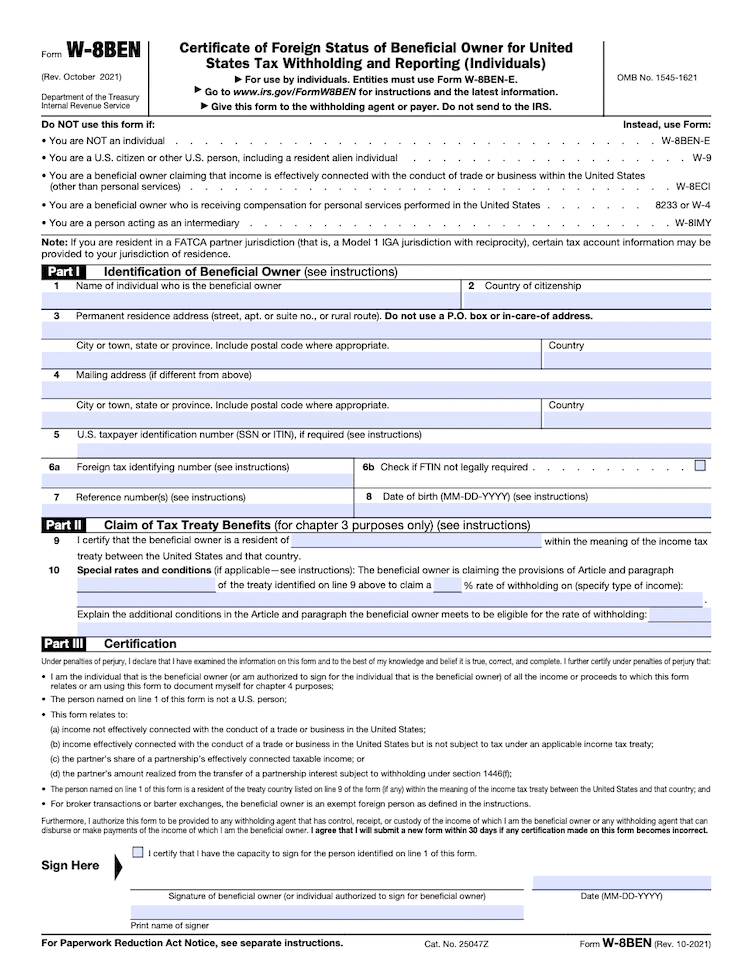

The W-8BEN and W-8BEN-E forms are United States tax forms that are typically completed by foreign individuals and entities, respectively who earn income from the U.S. These forms are crucial for establishing tax status and claiming treaty benefits.

For individuals Form W-8BEN, Line 9 needs to list the treaty country.

For entities using Form W-8BEN-E:

• Box 14b and Line 14b must indicate the applicable Limitation on Benefits (LOB) provision.

• Box 14a and Line 14a should identify the treaty country.

However, these are just the basics. Additional conditions may apply depending on the type of income involved—be it interest, dividends, royalties, or business profits.

Beyond the Basics: Special Cases

It’s essential to delve deeper into the unique requirements for different types of income. For instance, if a corporation claims treaty benefits for business profits, Line 15 of the W-8BEN-E form becomes critical. Royalties may also require different withholding rates, as seen in the U.S.-Canada tax treaty, necessitating detailed certifications on the type of royalty income.

Understanding IRS Scrutiny: U.S.-India Tax Treaty

The IRS has started putting more emphasis on the validity of business profits treaty claims. A notable case is Article 12 of the U.S.-India tax treaty. The IRS now asserts that IT services provided by Indian companies to U.S. clients are subject to 15% withholding, even if it seems this is a standard business profit situation. Therefore, withholding agents should review payments carefully, perhaps even maintaining multiple W-8 forms to cover various scenarios.

Treaty Mismatches and Curing Documentation

When validating a treaty claim, withholding agents conduct a meticulous review. Any discrepancy between claimed treaty jurisdiction and permanent or mailing addresses can lead to enhanced IRS scrutiny. Curing documentation may be necessary to establish residency in the treaty country and will go beyond merely showing a passport. Documents such as a residency permit or a driver’s license may be required.

Common Pitfalls and FAQs

- Incomplete Treaty Benefits Section: Simply having an address in a treaty country is not enough to claim benefits. An incomplete or inaccurate form can lead to under-withholding, penalties, and interest.

- Indefinite Validity: Forms W-8 with treaty claims are not eligible for indefinite validity, contrary to popular belief.

- Invalid Treaty Claims: An invalid treaty claim does not make the whole Form W-8 invalid. It can still be used for other purposes, such as establishing foreign status.

Conclusion

The stakes are high, especially with the IRS becoming more stringent. If you are dealing with cross-border transactions involving the U.S., it is important to consult an experienced international tax attorney for personalized guidance. Whether an individual or a corporation, understanding the nuances of W-8 forms and treaty claims can significantly impact tax situations, making it essential to get it right the first time.

Before ticking off boxes on W-8 forms, be sure to understand what each box entails, and when in doubt, seek professional advice. When it comes to international taxation, it is always better to be safe than sorry.

Leave a Reply