Federal Tobacco Taxes

In the installment of our Tax and Vice blog, we discuss California State (CDTFA) Federal Tobacco Excise Taxes. The Alcohol and Tobacco Tax and Trade Bureau (TTB) is responsible for collecting Federal Tobacco Taxes, not the IRS. The CDTFA collects state excise taxes in California. This post will provide a basic rundown of federal tobacco excise taxes and California (CDTFA) tobacco excise taxes. We will also discuss TTB Tobacco Tax audits of Tobacco Manufacturers and Tobacco Importers and CDTFA audits of tobacco manufacturers, importers, wholesalers and distributors.

As usual, we give our standard disclaimer concerning this blog. We are not trying to be “holier than thou,” so please do not give us a hard time if you see one of us puffing on a cigar or using other tobacco products. We also acknowledge tobacco use has health risks. We encourage everyone to make responsible and well-informed choices with regards to tobacco and other lifestyle choices.

The federal government imposes excise taxes on tobacco. The current rates can be viewed on the TTB’s website. The tobacco excise tax covers products like cigarettes, cigars, pipe tobacco, and snuff. Electronic cigarettes or vapes are currently not subject to the federal excise tax.

The federal tobacco excise tax is paid by tobacco manufacturers and importers. The Tax is generally due when tobacco is removed from the facility of a tobacco manufacturer or importer. There are some exceptions such as a tobacco that is exported outside the United States.

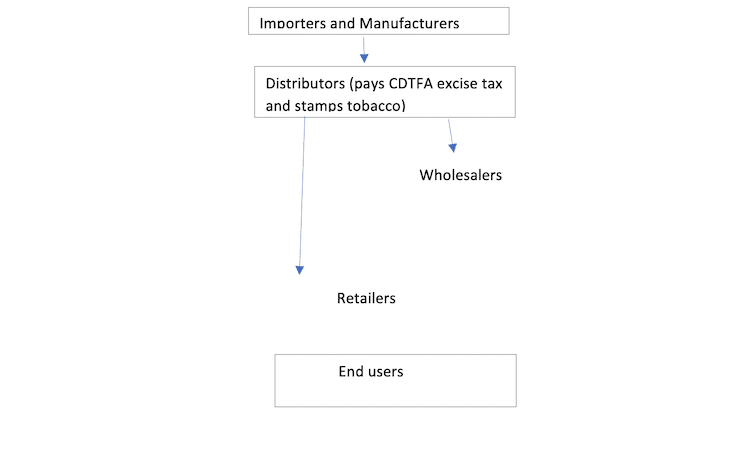

Many states like California may impose state excise taxes on electronic cigarettes or vapes. California imposes excise taxes on tobacco distributors. The California statute views the tobacco distribution chain as consisting of four tiers: (1) manufacturers and importers, (2) distributors, (3) wholesalers, and (4) retailers. Tobacco excise taxes are paid by distributors

Importers and manufacturers distribute tobacco to distributors. The distributors pay tax on the tobacco they distribute to wholesalers and retailers and stamp the tobacco. Wholesalers distribute stamped tobacco to retailers. Retailers distribute tobacco to end users. Manufacturers, importers, wholesalers, and distributors are required to file returns with the CDTFA even though only distributors pay tax.

The TTB requires tobacco manufacturers and tobacco importers to keep extensive and detailed records. These records include records of all tobacco coming into the facility and detailed invoices of all tobacco removed from the facility. The CDTFA has similarly stringent requirements. The CDTFA requires all tobacco sold in the state to list the recipient’s permit number. Failing to have proper documentation can pose serious problems at a TTB Audit or CDTFA Tobacco tax audit.

RJS LAW helps tobacco manufacturers, importers, distributors, wholesalers, and retailers with TTB and CDTFA audits. Please reach out to us if you have questions regarding tobacco taxes or if you need representation during an audit.

Written by Joseph Cole, Esq., LL.M.

Leave a Reply