You are the Boss and We Help Bosses – A California Employer’s Guide to Payroll Taxes

Insights from an EDD Audit Attorney

Part 2 – Trust Fund Recovery Penalties

This next installment of or Payroll Tax Blog will discuss Trust Fund Recovery Penalties. Trust Fund Recovery Penalties are penalties assessed against individuals for businesses’ failures to pay payroll taxes. As an EDD Audit Attorney, I have encountered countless Trust Fund Recovery Penalty Cases. Trust fund recovery penalties are based on the “trust fund” portion of the taxes an employer withholds from their employees’ paychecks. This blog will discuss what the trust fund portion of the taxes are, who gets assessed, and how the IRS and EDD audit, and investigate trust fund recovery penalties.

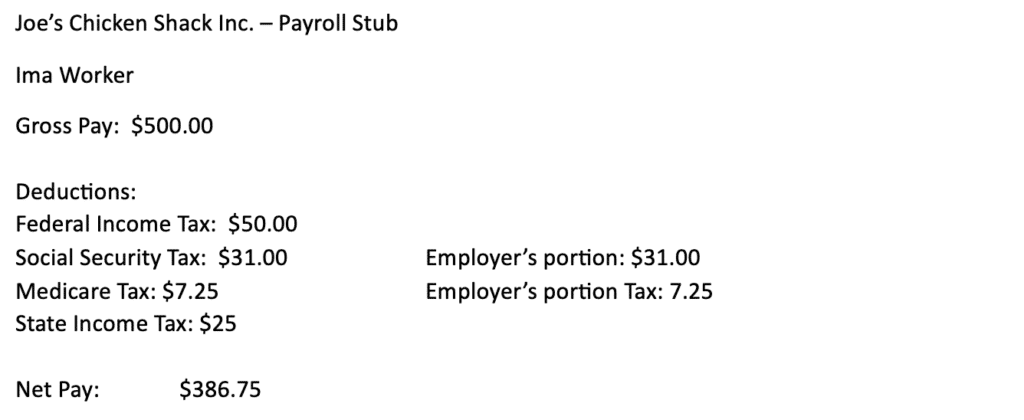

Above is a pay stub for a worker earning $500 gross pay during a particular pay period. After payroll related taxes withheld by the employer, the worker’s take home pay is $386.75.

If we assume the above worker is the business’ only employee, the employer’s total federal payroll tax liability will be $126.50. This consists of the federal tax liability ($50.00), both halves of the Social Security tax ($62.00 total), and both halves of the Medicare tax ($14.50 total).

The trust fund portion consists of the taxes withheld from the check. The federal trust fund portion of the check of the tax is $88.25. The federal trust fund portion consists of $50.00 federal income tax withheld from the check, $31.00 for social security tax withheld, and $7.25 for Medicare Tax withheld. For state tax purposes, the state trust fund portion is $25.

The above employer is a corporation. The IRS (and state agencies such as the California EDD) may pursue individuals for the trust fund portion of employment taxes. That is to say they will hold individuals personally liable for the trust fund portion of taxes owed by corporations, LLC’s, and other business entities.

Whether an individual should be personally responsible for the trust fund recovery penalty is a two- part inquiry. The first part of the inquiry is whether the person was a responsible person in a position of authority over the business’ finances. Generally speaking, a high-ranking officer like a CEO would be considered a responsible person. In a closely held business, the owners will usually be considered responsible persons as well. There can be some controversy as to whether certain other individuals such as bookkeepers, certain investors, and certain managers of a business are responsible persons for payroll tax purposes.

The second part of the test is whether the person behaved willfully. The term willfully is often misunderstood. It does not necessarily mean the people in control of the business acted fraudulently or in bad faith. It simply means the responsible people used trust funds, supposedly withheld from an employee’s paycheck, and spent those funds on anything other than paying payroll taxes.

To give an example of a typical case we come across, let us say a particular business owner is a model citizen who always paid her taxes. She faced some cash flow issues (as almost all businesses owners do at one point or another) due to challenges a business owner may face such as unfavorable market conditions, supply chain issues, losing a key customer, dealing with an illness, or experiencing some sort of natural disaster. She is faced with some difficult financial decisions and is stuck between a rock and a hard place. Rather than see her business shut its doors and put tis workers out of a job she makes the difficult decision to forego paying her payroll taxes so she can pay her employees, suppliers, or other required business expenses.

We can all certainly empathize with the above business owner. Perhaps we would do the exact same thing in her position. (As a tax attorney all I could do is advise her to pay her taxes). No doubt she had the best intentions. Nevertheless, she will be deemed to have acted willfully as she took money from the employees’ paychecks and applied it elsewhere. As such, she would be liable for the trust fund recovery penalty.

When a business owes payroll taxes, the IRS typically sends a field agent called a Revenue Officer to investigate a business. The Revenue Officer will conduct a 4180 interview with the individuals the Revenue Officer suspects may be in charge of a business. (It is called a 4180 interview because the IRS has the interviewees fill out a Form 4180). During a 4180 interview, a Revenue Officer will ask questions like which individuals had financial control over the business and who had control over the bank accounts.

IRS Revenue Officers often obtain bank signature cards and cancelled checks to determine which individuals were signing checks (and hence making financial decisions) for a business. While appearing on a bank signature card should not be automatic grounds for a trust fund recovery penalty assessment, some IRS Revenue Officers have been known to use bank signature cards as a litmus test for trust fund recovery penalty liability.

At the conclusion of the 4180 interview and Revenue Officer’s investigation, the Revenue Officer should issue a Letter 1153 to the individuals being assessed with a Trust Fund Recovery Penalty. The individuals generally have 60 days to file an appeal to the Trust Fund Recovery Penalty and have their appeal heard by the IRS Office of Appeals. The Individuals may also file for a refund suit in District Court if they pay an amount equal to the trust fund portion of a single employee’s paycheck for each quarter.

At the end of the process, a business owing payroll taxes will have to make some sort of payment arrangement for the payroll taxes owed. The individuals who had trust fund recovery penalties assessed against them may also have to make payment arrangements with the IRS. These payment arrangements can be some sort of installment agreement, obtaining a Currently Non-Collectible Status, or possibly arranging an Offer in Compromise with the IRS.

At RJS LAW – You are the Boss and we help bosses. We routinely assist businesses and their owners who have IRS and EDD payroll tax issues. If you or your business have payroll tax issues, call an experienced EDD audit attorney at 619-595-1655 or contact RJS LAW online today.

Written by Joseph Cole, Esq., LL.M. – EDD Audit Attorney

Leave a Reply