IRS Form 8300

If you engage in a business or trade that receives large cash payments, understanding IRS Form 8300 – what it is and why is it important – is crucial. The IRS mandates “each person engaged in a trade or business who, in the course of that trade or business, receives more than $10,000 in cash in one transaction or two or more related transactions, must file a Form 8300.”

What does Related Mean in the Context of Transactions?

Related has two possible meanings. One meaning is multiple transactions occurring between a payer and recipient of cash within 24 hours. To illustrate, imagine you are a retail dealer of lawn tractors. You sell Jack a tractor for $9,000 this morning. Jack pays in cash. Realizing he needs more equipment, Jack returns later that afternoon and purchases additional equipment for $4,000, again paying in cash. These would be considered related transactions as the multiple transactions occurred between the payer and recipient within 24 hours. As a result, these cash payments would be aggregated and necessitate the reporting of the transactions via Form 8300.

Another meaning of related is multiple transactions occurring over more than 24 hours in which the cash recipient knows the transaction is part of a series of connected transactions. For example, imagine you completed an $11,000 project for a customer of your business. Your customer wishes to pay you in two separate cash payments, to which you agree. You receive $5,000 of partial payment in cash from your customer today, and $6,000 in cash two days later. These would likely be considered related transactions and require reporting on Form 8300.

Penalties

There is a minimum penalty of $25,000 if the IRS determines there was an intentional or willful disregard of the reporting requirement. Additional violations related to the use, completion, and reporting requirements of this form may result in criminal prosecution. As such, it is crucial to ensure you not only file a Form 8300 when required, but that the information on the form is complete and correct.

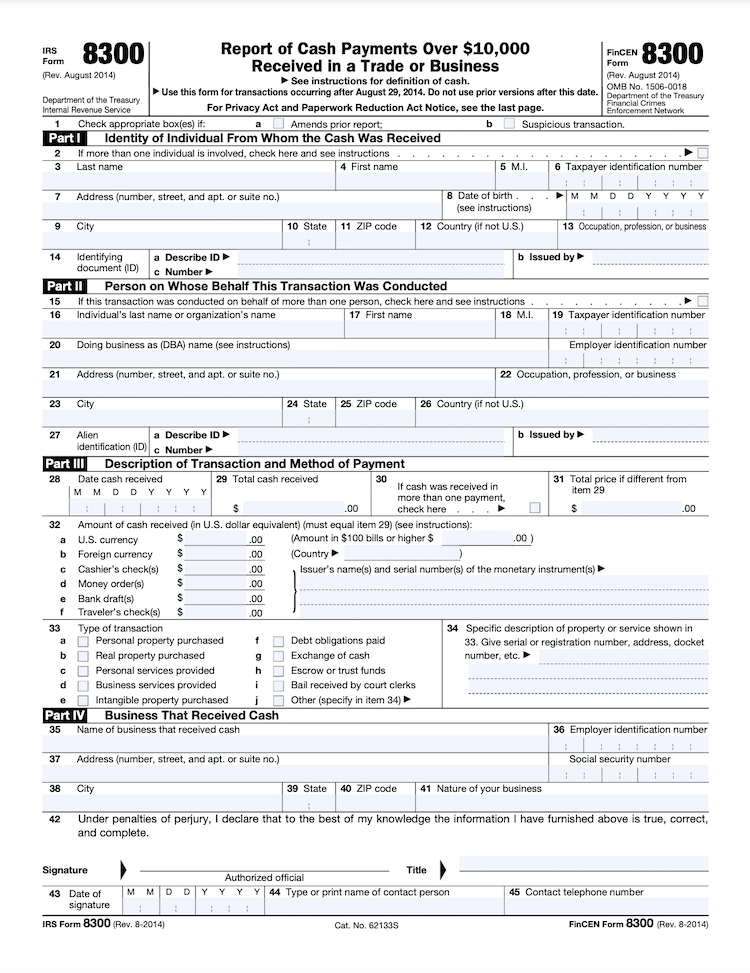

Required Information on Form 8300

The IRS states the entire form must be completed. We will highlight some of the key fields and information required in the form’s four parts on the first page. Please note this discussion is not exhaustive and does not include every field. We encourage and advise Form 8300 filers to thoroughly read and review the accompanying instructions before completing and filing the form.

Part I: Identity of the Individual from Whom Cash Was Received

In this part, you identify the person from whom you received cash. You will be required to document the name, Taxpayer Identification Number (TIN), address, date of birth, occupation, and details from an identifying document of the person from whom you collected the cash.

Per the IRS, if you have attempted to obtain the TIN but have not been able to get it within the 15 days following the transaction, you should still file the report. However, you should use the Comments section on the second page of the form to explain why the TIN is missing. There are other exceptions for when a TIN may not be required. We recommend reviewing the instructions for more details to determine if those instances apply to your situation.

Part II: Person on Whose Behalf This Transaction Was Completed

This section should be completed if the transaction was conducted on behalf of a person or organization. Please view the fields and instructions on Form 8300 as needed if this applies to your transaction.

Part III: Description of Transaction and Method of Payment

Here, you will need to document items such as the date the cash was received, the amount received, and whether the cash was received in more than one payment. There are additional fields in this part that need to be filled out; be sure to thoroughly read the form so that you know what information to record.

Part IV: Business That Received Cash

Enter the details of your business that received the cash. Sign and date the form indicating that the information provided is true, correct, and complete.

Additional Items

There is a second page of Form 8300—composed of two parts, I and II— to be completed if Box 2 or Box 15 is checked on the first page. Ordinarily, these parts are applicable only if multiple parties participated in the transaction.

The other pertinent part of the second page is the Comments section. This section is used as a supplement to comment on or clarify information. For example, this section should be used if you were unable to obtain and include the TIN in the form, or if reporting a suspicious transaction.

When to File

Form 8300 must be filed by the 15th day following the date the cash was received. If the 15th day falls on a weekend or holiday, the form must be filed on the next business day after the weekend day or holiday. Keep a copy of the submitted Form 8300 for 5 years.

How to File

Paper: Form 8300 may be mailed to the IRS at the following address:

IRS

Detroit Computing Center

P.O. Box 32621

Detroit, MI 48232

Electronic: As an alternative to the paper filing, you can e-file Form 8300 at http://bsaefiling.fincen.treas.gov/main.html. This utilizes the Financial Crimes Enforcement Network (FinCen)’s Bank Secrecy Act (BSA) E-Filing system. One benefit of e-filing is instant confirmation of submission.

Follow up after Filing

You are required to provide a written or electronic statement to each person named on a Form 8300 no later than January 31 of the year following the year in which the cash was received. This statement must list the name, address, and phone number of the business that received the cash, as well as the aggregate amount of cash received. Additionally, the notice must state that this information was sent to the IRS. Note, a statement is not required when Form 8300 is filed to report a suspicious transaction.

An Example of Timing

For example, imagine that you received $12,500 cash as payment for the services of your business. You received the cash on July 1, 2023. This means you would have until July 17, 2023, to file Form 8300 (as July 16 is a Sunday). Then, you would have until January 31, 2024, to send a written or electronic statement to each person named on the form. You should also retain a copy of the form and subsequent individual notices until July 17, 2028.

Additional Notes about Form 8300

- The IRS requires completing the entire form and recommends marking an item as “None” or “N/A” if it does not apply to your situation. By doing so, you reduce the risk of the IRS thinking you overlooked an item.

- A transaction is reportable only if it is in the course of the person’s trade or business.

- Form 8300 may be voluntarily filed for any suspicious transaction, even if the amount of cash received is less than $10,000. If you are filing Form 8300 for a suspicious transaction, be sure to check Box 1b near the top of the first page.

- The IRS has established a dedicated Form 8300 Helpline. This line is available Monday-Friday from 8:00am-4:30pm EST and is staffed by trained specialists to answer general questions about methods and filing requirements. The Form 8300 Helpline can be reached by calling 866-270-0733 from within the United States, or 313-234-6146 if calling from outside the United States.

- Questions on e-filing may be directed to the BSA E-Filing Help Desk at 866-346-9478 or email BSAEFilingHelp@fincen.gov.

If you are involved in a business or trade and receive payments of more than $10,000 in cash, we encourage you to familiarize yourself with Form 8300 so you remain compliant with IRS regulations. For questions regarding Form 8300 or any tax-related issues and regulations, please contact us at (619) 595-1655 for a free consultation. The team of experienced Tax Law Attorneys at RJS LAW looks forward to assisting you.

Written by Charles Ecker

Leave a Reply